Inside The Baltic Defence Tech Landscape

Most maps of European defence start with the big primes and the big capitals. We wanted to start somewhere else: with the three countries that have spent the last decade quietly turning necessity into capability.

Together with Dealroom, we've mapped the Baltic Defence ecosystem - 200 companies across Estonia, Latvia, and Lithuania. It is not a list of weapons manufacturers. It's a picture of a whole ecosystem: the firms building military equipment, the dual-use startups whose technology also strengthens defence, the infrastructure operators everyone else depends on, the government and border-security vendors, and the voices of associations and the ecosystem that hold it all together.

This piece explores what the current landscape looks like, why the region deserves your attention right now, and where each country is genuinely strong - including what's coming over the next few years. Everything presented here is based on publicly available information. We've tried not to overstate anything. The Baltic defence-tech scene is young. But the direction is hard to miss.

Why the Baltics, and why now

The commonly heard story about the Baltics is one of fear. We don't think that's the right one - and it isn't what the numbers actually show. What the numbers show is conviction: three governments making long-term, structural commitments to defence, and an investment environment that has become unusually predictable as a result.

Start with spending. All three Baltic states have committed to defence budgets of around 5% of GDP from 2026 - well ahead of the rest of the alliance. Estonia is committed to allocating roughly 5.4% of GDP annually to defence from 2026 to 2029. Lithuania is already spending around 5.4% of its GDP, almost three times its 2019 level, and Latvia is close behind at roughly 4.9%. For context on how far ahead that is: at the June 2025 NATO summit in The Hague, the allies adopted a new investment plan committing to 5% of GDP by 2035. The Baltics aim to be there nearly a decade early.

For anyone building or investing in this sector, that matters for one simple reason: it makes demand predictable. A defence budget locked in at 5% of GDP across a multi-year horizon is the kind of forward visibility most markets can't offer. The alliance-wide target itself is now formally split into 3.5% for core defence and 1.5% for security and resilience - a structure that explicitly rewards the dual-use, infrastructure, and innovation work this region specialises in.

The money is increasingly backed by shared European machinery, too. In May 2025 the EU adopted the SAFE instrument, providing up to €150 billion in loans to help member states scale defence investment through common procurement. It's the first pillar of a wider plan - ReArm Europe / Readiness 2030, aiming to leverage over €800 billion. When the Commission announced its tentative allocations in September 2025, 19 member states had already expressed interest, seeking support beyond the available budget. And the longer-term pipeline is growing as well: the European Defence Fund, the EU's dedicated defence R&D instrument worth nearly €7.3 billion for 2021-27, received a €1.5 billion top-up at the budget's mid-term review, and the Commission has proposed €131 billion for defence and space in the next seven-year EU budget - roughly five times current levels. Frontline states bordering Russia are squarely among the intended beneficiaries.

Then there's a second advantage that's easy to overlook: speed of feedback. Because these are small, tightly connected countries with engaged defence establishments, the distance between a startup and an actual end-user is short. Estonia's NATO DIANA accelerator describes this directly - everyone is one call away, and companies can find VCs and defence end-users at the same event. For a dual-use company, that's a structural gift: you can test, get feedback, and iterate against real operational requirements without crossing an ocean.

And it's all anchored in NATO and the EU. The Baltic region is not an isolated frontier; it's allied territory with a deepening allied presence. Germany, for example, has now stood up its 45th Armoured Brigade in Lithuania - around 4,800 troops, fully operational by 2027, its first permanent foreign troop deployment since the Second World War. That kind of commitment is, in the most practical sense, infrastructure: it's what makes long-term investment in the region credible rather than risky.

Put those four things together - predictable demand, European co-financing, fast feedback loops, and NATO/EU anchoring - and you have the real case for the Baltics. Not a region reacting to threat, but a region that has made security a durable, well-funded national priority, and built an environment where defence and dual-use technology can be validated before it scales internationally.

How we built the landscape

A lot of "defence" maps only count companies whose product is a weapon. That misses most of what actually makes a defence ecosystem work. Modern defence runs on software, sensors, communications, energy, logistics, and the institutions that fund and certify all of it. So we used a broader frame.

The following classifications and all company counts come from our landscape dataset.

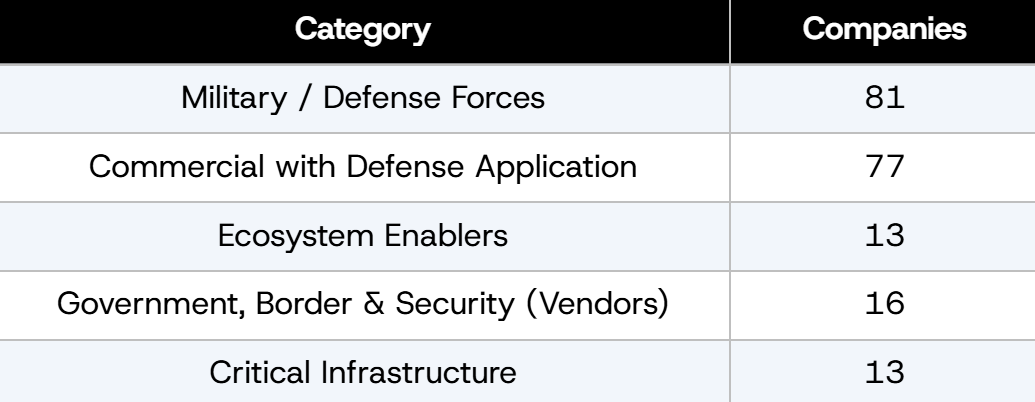

We sorted all 200 companies into five categories:

• Military / Defense Forces - companies whose main business is selling to armed forces: weapons and ammunition, drones and counter-drone systems, armoured vehicles, military robotics, soldier kit, and the firms that maintain that equipment. If the army is the main buyer, the company sits here.

• Commercial with Defense Application - normal commercial businesses serving mostly civilian or industrial customers, but whose products are also useful for defence. Dual-use drones, lasers and optics, metalworking and electronics subcontractors, IT and software firms. Defence is one part of the business, not all of it.

• Ecosystem Enablers - not product companies at all. Industry associations and clusters, government funds, accelerators and incubators, universities and research institutes, testing and certification bodies. They fund, train, connect, and certify others.

• Government, Border & Security (Vendors) - companies selling mainly to non-military government security buyers: border and coast guards, police, customs, intelligence, and national cyber agencies.

• Critical Infrastructure - the organisations that actually run a country's essential systems: electricity and gas grids, telecoms, railways, broadcasting. These are the operators, not vendors selling to them.

The point of the broader frame is honesty. A real ecosystem needs all five layers - including the subcontractors and enablers that rarely make headlines. Mapping only the weapons makers would have given you a highlight reel, not a map.

What the data shows

Everything in this section comes from our landscape dataset of 200 companies.

The first thing that stands out is that this is a genuinely three-country ecosystem, not one hub with two satellites. By country of origin: Estonia leads with 83 companies, Lithuania has 55, and Latvia has 47. The remaining 15 are foreign-headquartered firms with a presence in the region - more on those shortly.

The category split tells you how broad the base is:

What's striking is the balance between the top two: 81 companies sell primarily to defence forces, and another 77 are dual-use - civilian-first businesses whose technology also serves defence. That near-even split is the signal worth dwelling on, because it changes what kind of market this is. Dual-use companies give the ecosystem two engines: commercial revenue keeps them alive between procurement cycles, while defence demand pulls their technology up the readiness curve. For investors, that means venture-style outcomes don't depend on government contracts alone; for the armed forces, it means a far wider supplier base to draw on than the formal defence industry. So this isn't a pure arms cluster, and it isn't pure dual-use either. It's both at once.

Underneath both groups sits a layer of 13 ecosystem enablers - funds, clusters, accelerators, universities, and research institutes. That works out to roughly one enabling institution for every fifteen companies on the map, and it goes a long way towards explaining why the feedback loops described earlier are as short as they are.

The ecosystem is also overwhelmingly home-grown. Of the 200 companies, 185 originate in the three Baltic states - evidence of organic depth rather than a market propped up by visiting primes. The 15 foreign entrants are a meaningful minority, not the foundation.

Just as telling, these companies don't stay inside their own borders. Counting where companies have an operational presence, our data records 97 company-presences in Estonia, 68 in Lithuania, and 59 in Latvia - with a number of firms active across all three states. In practice, that means a company can treat the Baltics as closer to one connected market than three separate small ones.

Look one level deeper and the three countries' profiles diverge in instructive ways. Estonia's map skews commercial: 37 of its 83 companies - around 45% - are dual-use businesses, and it hosts nearly half of the region's ecosystem enablers (6 of the 13), consistent with its startup-economy DNA. Latvia leans the other way: just under half of its 47 companies sell primarily to defence forces, and it is home to most of the critical-infrastructure operators on the map (6 of the 13) - a more defence- and resilience-weighted mix. Lithuania sits between the two, pairing 22 direct defence suppliers with a 21-company dual-use industrial base built around its photonics and precision-manufacturing supply chain. In other words, the three markets aren't smaller copies of each other - they're different layers of the same stack, which is precisely what makes the region work as one platform.

The growth behind these numbers hasn't been accidental, either - each country has built its own machinery for it, and European money increasingly flows through that machinery. Lithuania's defence ministry doubled its Defence Technology Development Programme to €5 million, using it partly to co-finance European Defence Fund projects - one reason laser firm Altechna Sensing now sits inside the EDF's project to develop a 100 kW-class laser weapon. Latvia's Origin Robotics won €4.5 million from the same fund for unmanned targeting technology, and its BLAZE interceptor is now among the systems Latvia is procuring with money from the EU's new SAFE instrument - a clean example of European mechanisms carrying a local company from R&D to fielded product. Estonia, for its part, pairs European programmes with state capital of its own, as the next section shows. Different approaches - co-financing, flagship projects, state funds - but the same effect: EU instruments are not abstractions here. They are how companies on this map are actually scaling.

A note on funding and value

A word on what we can and can't say about money. Comprehensive funding and valuation data does not exist for most of these 200 companies - many are privately held, early-stage, or have never raised external capital - so we are not going to put a single headline number on the size of the industry. That figure would be a guess dressed up as a fact. What we can do is point to the publicly disclosed numbers for the companies large enough to have them, which gives an honest sense of the ceiling this ecosystem is already reaching.

The standout is Estonia's Skeleton Technologies, the energy-storage and supercapacitor maker, which has raised roughly €392 million to date and is targeting a US listing in 2027 - among the best-funded deep-tech companies in Europe. A second reference point is Helsing, the AI-defence company that is German-headquartered but runs an Estonian subsidiary and sits on this map as a foreign entrant: it has raised about €1.37 billion and was valued at €12 billion in mid-2025.

And exits are happening: in 2023 Estonia's Milrem Robotics was acquired by the UAE's EDGE Group in what was described as the largest foreign investment in Estonia's defence sector. These are the outliers, not the median - but they show that companies from this region can reach European and global scale.

Latvia offers its own example of scale in the wider technology base: networking-equipment maker MikroTik reported turnover of around €327 million in 2024, making it one of the country's largest technology firms, while SAF Tehnika has been listed on Nasdaq Riga since 2004. Most of these are dual-use businesses rather than pure defence plays, which is exactly the point: the commercial base the defence ecosystem draws on is already substantial.

Where each country is strong

No single Baltic state is trying to do everything, and that's a strength. Each has a distinct speciality, and together they're complementary - optics, software, and communications form a coherent regional value chain rather than three competing ones. Company examples below are drawn from our landscape; market figures and recent news are linked to public sources.

Lithuania - the photonics powerhouse

The unique selling point: Lithuania isn't just good at lasers - it's a genuine world leader. The country's photonics sector has grown around 16% a year over the past decade, roughly ten times the European average, and a single Lithuanian firm, Light Conversion, holds about 80% of the global market for tunable femtosecond lasers. Lithuanian laser systems are used in 95 of the world's top 100 universities. For a country of under three million people, that is an extraordinary base to build defence capability on.

Current strengths (from our landscape): around a dozen Lithuanian companies and institutions work in optics, lasers, and photonics - among them Eksma Optics, Altechna, Optoman, Optogama, and Femtika on components and laser systems, Brolis Defence on the defence-specific end, and the FTMC research institute and the Lithuanian Laser Association anchoring the science and the cluster. Precision optics and electro-optical assemblies are exactly the dual-use building blocks that matter for sensing, targeting, and secure communications.

What's coming: two shifts are worth watching. First, the laser industry itself expects to grow roughly ten-fold by 2030, with defence and space called out as its most reliable growth markets. Second, Lithuania is now where the region's heaviest industrial bets are landing - Rheinmetall broke ground in November 2025 on a 155mm artillery plant, the largest defence investment in the country's history, a joint venture with state energy group EPSO-G worth up to €300 million, followed immediately by an MoU for a propellants Centre of Excellence. On the deep-tech side, Vilnius space-comms startup Astrolight raised €2.8 million in 2025 and field-tested unjammable ship-to-ship laser links with the Lithuanian Navy - with around 30% of Lithuanian space projects drawing EU funding, nearly double the EU average.

Estonia - the digital-defence pioneer

The unique selling point: Estonia turned an early wake-up call into a global niche. After the 2007 cyber-attacks, it became home to NATO's Cooperative Cyber Defence Centre of Excellence (CCDCOE) in Tallinn, which now runs Locked Shields - the world's largest live-fire cyber exercise, with around 4,000 experts from 41 nations. No other Baltic state has that kind of institutional gravity in a single domain. And in May 2024 NATO chose Tallinn for DIANA's European Regional Hub - making Estonia the innovation crossroads of the whole region.

Current strengths (from our landscape): Estonia's profile is digital-first - dense in software, cybersecurity, autonomy, robotics, and space and energy deep-tech. Firms include Nortal in digital transformation and cyber, Skeleton Technologies in advanced energy storage, and GaltTec in fuel-cell power, alongside a deep bench of dual-use software companies. The standout is Milrem Robotics, whose THeMIS unmanned ground vehicle is combat-proven and now operated by multiple armed forces.

What's coming: the trajectory is steep. Estonia's defence industry has grown nearly 350% since 2021, with exports forecast around $518 million for 2025, and the country is backing it with a €100 million state DefenceTech fund (via SmartCap) aiming to grow the sector from ~€500M to €2B by 2030. Milrem is moving from products to platforms and partnerships - including a 2026 cooperation with Poland's PGZ on autonomy and counter-drone systems, and Estonia's startup pipeline keeps converting: in late 2025 two Estonian firms were selected for Phase 2 of NATO DIANA from over 2,600 applicants.

Latvia - the drone and connectivity hub

The unique selling point: Latvia has turned itself into a convening power for European drones. It founded and leads the international Drone Coalition, now 20 member states strong - an initiative the defence ministry itself credits with turning Latvia into an international brand. The annual Riga Drone Summit has become a fixture, with its 2026 edition gathering coalition ministers and industry. Few states in Europe - of any size - own a Europe-wide defence initiative in this way.

Current strengths (from our landscape): Latvia clusters around communications, autonomous systems, language and AI technologies, and critical-infrastructure resilience. The landscape features SPH Engineering in drone software and mission planning, SUBMerge Baltic in autonomous underwater vehicles, and Tilde in machine translation and language AI for Baltic languages - with national operators anchoring the critical-infrastructure layer. National champion LMT sits at the centre of the defence-tech scene. The breakout name, though, is Origin Robotics. Its BLAZE interceptor goes straight at one of modern air defence's hardest economics problems: cheap attack drones are launched in mass precisely to exhaust defences built around missiles that cost orders of magnitude more per shot, and an autonomous interceptor drone flips that cost equation back in the defender's favour. In February 2026, Latvia, Estonia, and Belgium received their first BLAZE systems - becoming the first countries in Europe to field a fully autonomous interceptor-drone capability - delivered within months of order, rather than the years defence procurement usually takes.

What's coming: Latvia is moving from coordinator to builder. LMT now leads VANTAGE, a six-country European Defence Fund project (~€11 million) to develop a next-generation VTOL drone - and 2025 was Latvia's most successful EDF year yet, with funding up 50% on 2024. In September 2025 the country opened an Autonomous Systems Competence Center linking operational needs to procurement - the body now responsible for bringing BLAZE into service - and LMT has spent four years as integrator of NATO's DiBaX experiments in complex-environment drone operations. On the testing side, Latvia hosts a NATO DIANA test centre for 5G, AI, and big-data, built around the 5G defence testbed at Camp Adazi - giving companies based there a real home-soil advantage.

Foreign entrants and market validation

The clearest external signal that this market is being taken seriously is who's choosing to build here. The 15 foreign-origin companies are from our landscape; the investment details below are from public sources.

Our landscape captures global primes and scale-ups that already have a Baltic footprint - among them Rheinmetall, Lockheed Martin, KNDS (Krauss-Maffei Wegmann), Patria, Helsing, and EDGE Group. When companies of that calibre plant a flag, they're validating the market in a way no policy document can.

The most concrete recent example is Rheinmetall in Lithuania. In November 2025 the company broke ground on a 155mm artillery ammunition plant in Baisogala - up to €300 million, ~150 jobs, operational from mid-2026, described by Lithuanian officials as the largest defence-industry investment in the country's history. And it isn't a one-off: at the same time, Lithuania and Rheinmetall signed an MoU for a propellants Centre of Excellence, addressing what the company called a key bottleneck in Europe's powder supply.

Private capital is following the same logic. In late 2024 the NATO Innovation Fund made its first Baltic investment, backing Vilnius-based BSV Ventures - the fund is a standalone vehicle backed by 24 NATO allies, and it framed the move as confidence in transforming the Baltics into a global hub for deep-tech and dual-use innovation. The pattern across both public and private money is consistent: manufacturers are building production here, and investors are funding companies here - both reading the same signals about demand, talent, and political stability.

And the partnerships now run east as well as west. In June 2026, Latvia and Ukraine signed a comprehensive defence-cooperation agreement centred on drones - covering the transfer of Ukraine's battlefield expertise in unmanned systems and air defence, joint research and development, and possible co-production and localisation - following the drone agreement Ukraine had already concluded with Lithuania. For the companies on this map, agreements like these mean direct access to the fastest-moving body of drone-warfare experience in the world - and for Ukraine's partners, a route into the Baltic supplier base.

The Baltics as a defence-tech platform

It's tempting to look at Estonia, Latvia, and Lithuania as three small national markets. We'd argue that's the wrong unit of analysis.

What the landscape shows is closer to a single regional platform: 200 companies spanning weapons makers, dual-use startups, infrastructure operators, security vendors, and the funds and research institutions that connect them - overwhelmingly home-grown, increasingly cross-border, and now drawing serious commitment from international primes and NATO-backed capital. It sits inside the most predictable defence-demand environment in Europe, with EU co-financing on tap and allied forces on the ground. That platform is about to get denser still: the EU's planned "drone wall" and Eastern Flank Watch - first proposed by the Baltic states themselves - are expected to reach initial operational capability by late 2026, running alongside the Baltic Defence Line fortifications the three countries are already building. For the companies in this landscape, that is a multi-year pipeline of demand forming on their doorstep.

For a founder, that means short feedback loops, real public funding, and end-users who are reachable. For an investor, it means a region where dual-use technology can be tested and proven against genuine requirements before scaling outward. For a foreign defence company, it means a credible, well-located base inside NATO - with a domestic supply chain to plug into and a path to the wider Northern and Central European market.

The ecosystem is still maturing, and we won't pretend otherwise. But the foundations - talent, demand, capital, and political commitment - are now visibly in place. The Baltics aren't waiting to become a serious defence-tech region. On the evidence of this landscape, they already are one.

If this landscape is your market, we want to hear from you. Whether you're a founder building in the region, an investor mapping it, or a company weighing a Baltic entry - reach out to the Venture Faculty team. Explore the full 200-company landscape, challenge our read of it, and if your company belongs on the map and isn't there yet, tell us. This is a living document, and the next edition will be sharper with your input.

Authors: Analyst at Venture Faculty, Tomass Vilks & Founder of Proposal Peak, Edgars Poga